38 valuing zero coupon bonds

Valuation of Zero-Coupon Bonds - YouTube This video provides an explanation of a zero-coupon bond and proceeds to show how the value and yield are calculated using manual computations as well as with financial calculator (BA II Plus) and... Zero-Coupon Bond: Formula and Excel Calculator If the zero-coupon bond compounds semi-annually, the number of years until maturity must be multiplied by two to arrive at the total number of compounding periods (t). Zero-Coupon Bond Value Formula Price of Bond (PV) = FV / (1 + r) ^ t Where: PV = Present Value FV = Future Value r = Yield-to-Maturity (YTM) t = Number of Compounding Periods

› publication › 256241591_Sales(PDF) Sales Promotions - ResearchGate Jan 01, 2012 · Unlike direct mail, the Internet is a virtuall y zero-cost . communication vehicle. ... However, the time to clip and use th e coupon comes from the time devoted t o leisure.

Valuing zero coupon bonds

quizlet.com › 95524462 › cfa-53-introduction-toCFA 53: Introduction to Fixed-Income Valuation - Quizlet The spot curve, also known as the strip or zero curve, is the yield curve constructed from a sequence of yields-to-maturities on zero-coupon bonds. The par curve is a sequence of yields-to-maturity such that each bond is priced at par value. Solved 1. Valuing a Zero-Coupon Bond Assume the | Chegg.com Valuing a Zero-Coupon Bond Assume that you require a 14 percent return on a zero-coupon bond with a par value of $1,000 and six years to maturity. What is the price you should be willing to pay for this bond? (Pease note that you have to answer this two problems step by step not directly, as my professor want it step by step, please provide a ... Zero-Coupon Bond Value | Formula, Example, Analysis, Calculator The value of a zero-coupon bond is determined by its face value, maturity date, and the prevailing interest rate. The formula to calculate the value of a zero-coupon bond is. Price = M / (1+r)n. where: M = maturity value or face value of the bond. r = rate of interest required. n = number of years to maturity. 3.

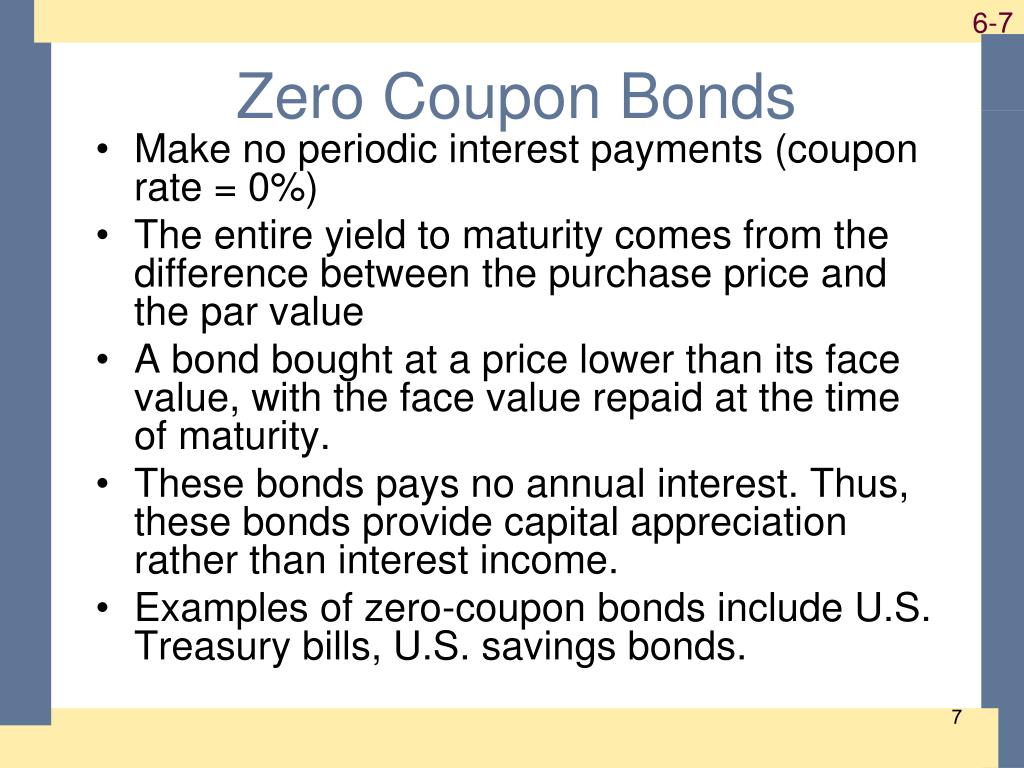

Valuing zero coupon bonds. Zero-Coupon Bond - Definition, How It Works, Formula To calculate the price of a zero-coupon bond, use the following formula: Where: Face value is the future value (maturity value) of the bond; r is the required rate of return or interest rate; and. n is the number of years until maturity. Note that the formula above assumes that the interest rate is compounded annually. Solved 2. Valuing a Zero-Coupon Bond. Assume the following | Chegg.com Valuing a Zero-Coupon Bond. Assume the following information for existing zero-coupon bonds: Par value = $100,000 Maturity = 3 years Required rate of return by investors = 12% How much should investors be willing to pay for these bonds? ANSWER: PV of Bond = PV of Coupon Payments + PV of Principal $0 + 100,000 (PVIF-12% -3) -$100,000.7118) -$71,180 PDF Numerical Example in Valuing Zero coupon Bonds For example, the value of a zero coupon bond will increase from $385.00 to $620.92 as the bond moves from 10 years to maturity to 5 years to maturity assuming interest rates remain at 10%. 4) Compare the value of the zero at 10 years to maturity when rates are 10% versus when they are 7%. Lower interest rates mean higher bond prices. Zero-Coupon Bond Definition - Investopedia The price of a zero-coupon bond can be calculated as: Price = M ÷ (1 + r) n where: M = Maturity value or face value of the bond r = required rate of interest n = number of years until maturity If...

How to Calculate the Price of Coupon Bond? - WallStreetMojo = $838.79. Therefore, each bond will be priced at $838.79 and said to be traded at a discount (bond price lower than par value) because the coupon rate Coupon Rate The coupon rate is the ROI (rate of interest) paid on the bond's face value by the bond's issuers. It determines the repayment amount made by GIS (guaranteed income security). Coupon Rate achieveressays.comAchiever Essays - Your favorite homework help service Your writers are very professional. All my papers have always met the paper requirements 100%. Value and Yield of a Zero-Coupon Bond | Formula & Example The forecasted yield on the bonds as at 31 December 20X3 is 6.8%. Find the value of the zero-coupon bond as at 31 December 2013 and Andrews expected income for the financial year 20X3 from the bonds. Value of Total Holding = 100 × $553.17 = $55,317 Expected accrued income = Value at the end of a period − Value at the start of a period Valuing Bonds | Boundless Accounting | | Course Hero Formula for Calculating Value of Zero-Coupon Bond Zero-Coupon Bond Value = Face Value of Bond / (1+ interest Rate) Generally, the price of a zero-coupon bond is based on the present value of the amount the issuing business will pay the bondholder when the bond matures. The amount the company pays at the end of the term equals the bond's face value.

Zero Coupon Bond - YouTube An example of pricing a zero-coupon bond using the 5-key approach. Valuing a zero-coupon bond | Mastering Python for Finance A zero-coupon bond can be valued as follows: Here, is the annually compounded yield or rate of the bond, and is the time remaining to the maturity of the bond. Let's take a look at an example of a 5-year zero-coupon bond with a face value of $100. The yield is 5 percent, compounded annually. The price can be calculated as follows: Zero Coupon Bonds Explained (With Examples) - Fervent | Finance Courses ... The value of a zero coupon bond is nothing but the Present Value of its Par Value. Zero Coupon Bond Example Valuation (Swindon Plc) Consider an example of Swindon PLC, which is issuing a zero coupon bond with a par value of £100 to be paid in one year's time. What is the price of this bond today, if the yield is 7%? Valuing a zero-coupon bond | Mastering Python for Finance - Second Edition Zero-coupon bonds are also called pure discount bonds. A zero-coupon bond can be valued as follows: Here, y is the annually-compounded yield or rate of the bond, and t is the time remaining to the maturity of the bond. Let's take a look at an example of a five-year zero-coupon bond with a face value of $ 100. The yield is 5%, compounded annually.

FRL 483 Doc 1 - Chapter 8 Bond Valuation and Risk 1 The appropriate ...

Arbitrage-free Valuation Approach for Bonds - Finance Train Let's take another example. Suppose we have a bond that matures in 2 years, that has a coupon rate of 6%, and pays coupon semi-annually. The spot rates are 3.9% for 6 months, 4% for 1 year, 4.15% for 1.5 years, and 4.3% for 2 years. The cash flows from this bond are $30, $30, $30, and $1030. The value of the bond will be calculated as follows:

Bonds

PDF Valuation of zero coupon bonds using Excel - CROSBI in general and especially in the case of zero coupon bonds. Besides that, very good books about Using Excel in Finance and Business do exist. [1] [11] [13] For valuation of zero coupon bonds (zero bonds) in this article, the basics of ordinary or coupon bearing bonds will be presented first and after that the case of

PPT - Chapter 5 PowerPoint Presentation, free download - ID:2441276

Zero-Coupon Bonds - Acing Finance Valuing Zero-Coupon Bonds To find the present value of a zero-coupon bond, we take the face value and divide it by the interest rate to the power of time to maturity. The formula is Where r is the interest rate, and t is the time to maturity. Example: A 3-year zero-coupon bond is issued with a face value of $1000 and an interest rate of 8%.

Zero coupon bond yield to maturity calculator 778066-Coupon bond yield ...

› an › enBond valuation and bond yields | P4 Advanced Financial ... The plain vanilla bond with annual coupon payments in the above example is the simpler type of bond. In addition to the plain vanilla bond, candidates – as part of their Advanced Financial Management studies and exam – are required to have knowledge of, and be able to deal with, more complicated bonds such as: bonds with coupon payments occurring more frequently than once a year ...

0 Coupon Bond Formula ~ coupon

Valuing a zero-coupon bond - Mastering Python for Finance [Book] A zero-coupon bond is a bond that does not pay any periodic interest except on maturity, where the principal or face value is repaid. Zero-coupon bonds are also called pure discount bonds. A zero-coupon bond can be valued as follows: Here, is the annually compounded yield or rate of the bond, and is the time remaining to the maturity of the bond.

Post a Comment for "38 valuing zero coupon bonds"